Chapter 7 Bankruptcy Attorney Tulsa for Dummies

Table of ContentsThe Chapter 13 Bankruptcy Lawyer Tulsa PDFsExcitement About Best Bankruptcy Attorney TulsaUnknown Facts About Bankruptcy Attorney Near Me TulsaNot known Incorrect Statements About Best Bankruptcy Attorney Tulsa 10 Simple Techniques For Tulsa Debt Relief Attorney

The statistics for the various other primary kind, Chapter 13, are even worse for pro se filers. (We damage down the differences in between the 2 key ins deepness listed below.) Suffice it to state, talk to an attorney or more near you who's experienced with insolvency regulation. Here are a few sources to discover them: It's reasonable that you may be reluctant to pay for an attorney when you're currently under significant financial stress.Lots of lawyers additionally use complimentary appointments or email Q&A s. Take benefit of that. (The non-profit app Upsolve can help you discover free examinations, resources and lawful help release of fee.) Ask them if personal bankruptcy is undoubtedly the appropriate selection for your situation and whether they assume you'll certify. Prior to you pay to submit bankruptcy forms and imperfection your debt record for up to 10 years, inspect to see if you have any kind of practical alternatives like debt arrangement or non-profit credit report counseling.

Ad Currently that you've chosen bankruptcy is without a doubt the ideal training course of activity and you ideally removed it with an attorney you'll need to get begun on the documentation. Before you dive into all the main bankruptcy forms, you should get your own documents in order.

6 Easy Facts About Chapter 13 Bankruptcy Lawyer Tulsa Shown

Later down the line, you'll really need to prove that by divulging all sorts of info about your economic events. Right here's a fundamental checklist of what you'll need when traveling ahead: Determining files like your vehicle driver's permit and Social Protection card Income tax return (as much as the previous four years) Proof of income (pay stubs, W-2s, self-employed incomes, earnings from assets as well as any type of earnings from federal government benefits) Bank declarations and/or retired life account statements Proof of worth of your possessions, such as lorry and property evaluation.

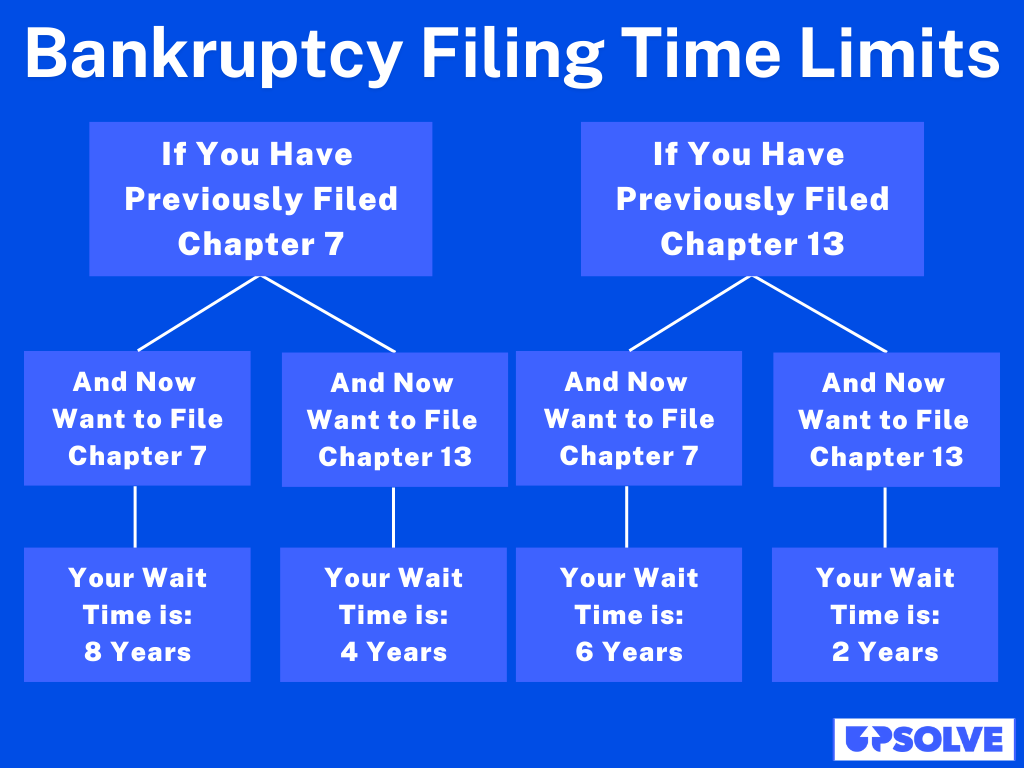

You'll wish to recognize what kind of debt you're trying to settle. Debts like child support, alimony and specific tax obligation financial debts can not be released (and bankruptcy can't halt wage garnishment associated to those financial debts). Pupil loan debt, on the various other hand, is possible to discharge, however keep in mind that it is hard to do so (Tulsa bankruptcy attorney).

You'll wish to recognize what kind of debt you're trying to settle. Debts like child support, alimony and specific tax obligation financial debts can not be released (and bankruptcy can't halt wage garnishment associated to those financial debts). Pupil loan debt, on the various other hand, is possible to discharge, however keep in mind that it is hard to do so (Tulsa bankruptcy attorney).If your revenue is too expensive, you have another option: Chapter 13. This option takes longer to settle your financial obligations due to the fact that it calls for a lasting settlement strategy generally three to 5 years before several of your continuing to be financial obligations are wiped away. The filing procedure is likewise a lot much more intricate than Phase 7.

Little Known Questions About Affordable Bankruptcy Lawyer Tulsa.

A Chapter 7 bankruptcy remains on your credit scores record for 10 years, whereas a Phase 13 bankruptcy falls off after 7. Before you submit your insolvency kinds, you should first complete a necessary training course from a credit scores therapy firm that has been accepted by the Division of Justice (with the notable exemption of filers in Alabama or North Carolina).

The training course can be finished visit the website online, in individual or over the phone. You should complete the program within 180 days of filing for personal bankruptcy.

4 Simple Techniques For Chapter 13 Bankruptcy Lawyer Tulsa

Check that you're filing with the proper one based on where you live. If your irreversible home has relocated within 180 days of filling, you should file in the area where you lived the higher section of that 180-day period.

Normally, your personal bankruptcy attorney will certainly work with the trustee, yet you might need to send the person records such as pay stubs, tax returns, and financial institution account and credit rating card declarations directly. A typical misunderstanding with insolvency is that when you submit, you can quit paying your financial obligations. While personal bankruptcy can help you clean out many of your unprotected financial debts, such as overdue medical bills or personal lendings, you'll want to keep paying your regular monthly settlements for protected financial debts if you desire to keep the property.

A Biased View of Tulsa Bankruptcy Attorney

If you go to threat of foreclosure and have tired all other financial-relief read this alternatives, then applying for Phase 13 may postpone the repossession and conserve your home. Ultimately, you will certainly still require the income to continue making future home mortgage repayments, along with repaying any late repayments over the program of your repayment strategy.

The audit might delay any type of debt alleviation by numerous weeks. That you made it this far in the process is a good sign at least some of your financial obligations are qualified for discharge.